Solicitors: Work areas attracting the most PII notifications

Published

Read time

It is 2024 and we are living in a post-pandemic world, with a difficult economic climate. We felt now would be a good time to consider whether these factors have had an impact on claims in the legal sector over the past four years.

With this in mind, we have taken the opportunity to review the notifications received by Howden over the 4 years from 2020 to 2023, in order to provide some insight to our clients in the legal sector. This includes a look at some of the changes we have seen in claims within certain work areas based on our claims data.

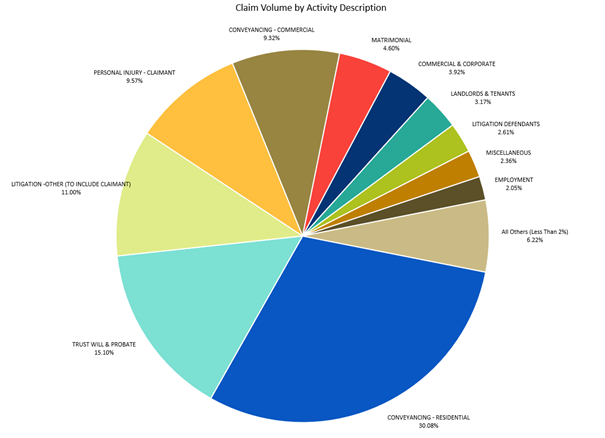

Key Work Types Giving Rise to Notifications

Over the past four years, the work areas in which we saw the highest number of professional negligence notifications have consistently been:

- Residential Conveyancing

- Trusts, Wills and Probate

- Personal Injury – Claimant

2020

2021

2022

2023

You will note that while the top three work areas generating claims remained the same over the past few years, the split altered slightly. Let’s look deeper in to the top three and some of the main causes of notifications.

Residential Conveyancing

Residential conveyancing generates the highest number of notifications to insurers. While there is good news in that the percentage of notifications has been decreasing over the last few years, there are some areas where we have seen an increase. The most notable changes evident from our data are:

- There has been an increase in claims and circumstances arising from failure to register the title or a charge over the past four years. There can be many reasons for this such as requisition deadlines being overlooked, transfers being drafted incorrectly or the omission to make an application to the Land Registry at all. The cause of these issues varies, but we recommend firms consider ways in which they could tighten up their risk management in this area.

- We have also seen an increase in notifications arising from boundary and right of way disputes. These notifications can arise as a result of anything from failing to include a separate title number in the transaction, to failing to highlight access issues or providing incorrect advice on easements in the title. Again, this is an area we would encourage conveyancers to ensure there is adequate review.

We had anticipated that there might be an increase in missed deadline claims in the residential conveyancing space – particularly at the end of the SDLT holiday and with the relentless and regular increases in mortgage rates. We expected that if deadlines were missed and a buyer did not achieve SDLT relief or had to pay a higher mortgage rate, they may claim against their conveyancer for the increased costs. However, our data does not show any evidence of this. We know that our clients were alive to these issues and we suspect that good risk management has helped to prevent such claims from arising.

Trusts, Wills and Probate

There has been little change to the cause of notifications in this area over the last four years, although we can see from our data that there has been an increase in the number of notifications, particularly regarding estate administration. One explanation for this is changes in the economy adversely impacting property and share values and prompting beneficiaries to allege loss if they can point to a delay in the administration of an estate.

Whilst we have seen an increase in claims relating to estate administration, claims relating to Will drafting have in fact decreased – which was an unexpected outcome. We anticipated that more claims might be made in this space as a result of an increase in hybrid and remote working, which could have led to difficulties with taking instructions during the covid-19 pandemic in particular. While we accept that it might be some time before such claims emerge and only time will tell, it is a case of “so far so good”.

The allegations made across Trusts, Wills and Probate primarily comprised:

- Drafting errors - meaning that the Will does not reflect the Testator’s wishes or that the Will drafting is ambiguous;

- Missing documents - such as the original Will of Power of Attorney going astray or;

- General breaches of duty when administering in the Estate – such as the failure to carry out instructions.

Typically, claims are pursued by disappointed beneficiaries and can become difficult to resolve due to complicated and sometimes acrimonious family history and the absence of the person who provided the original will instructions. With this in mind, it is imperative that firms have good file notes, correspondence and other relevant documentation to evidence their work and the instructions given.

Personal Injury Claims

Personal injury claims are generally one of the most common categories of litigation work conducted by lawyers, so it is expected that this work would account for a large number of PII notifications seen by insurers. The main reasons for notifications received were:

- Missed limitation dates;

- Other missed deadlines (e.g. failure to serve witness statement); and

- Errors in, or missing, documentation.

A key reason for missed limitation dates and other deadlines could be that, as with every profession, law firms are becoming more and more reliant on electronic diary systems and trusting that the system will flag the dates and deadlines to them. These issues could also be arising more frequently due to people changing the way they are working following the pandemic – and the increase in hybrid working in particular.

Unfortunately, in scenarios where deadlines are missed or documentation is missing, there are usually very limited arguments available to defend any claims that follow. We recommend it would be prudent for firms to consider how they can tighten up their internal procedures in order to avoid these scenarios and limit any potential exposure.

Some options to consider include:

- Whether key dates are recorded clearly on a file and if there is a reminder available for case handlers regularly informing them of such deadlines to limit the chances of these being missed;

- Is there any opportunity for a document checklist to be automatically flagged with the case handler to ensure all documents are completed before finalising or moving onto the next steps?

These are only two possible suggestions however, the important takeaway here is to ensure that risk management is robust and that there are as many safety nets as possible to avoid issues such as these which could lead to claims.

What proportion of notifications results in a payment?

The above chart shows notifications made from 2018 to 2023. For notifications that have closed it details those that involved payments (whether that be a claim payment and/or defence costs) and those that were closed without any payments at all. For open matters the chart shows those that have had payments made, or currently have reserves, and those that do not.

An important point to note is the “long tail” nature of notifications to solicitors’ PII insurer – that means the time it takes for matters that are notified to resolve and close. This makes it challenging for underwriters when it comes to pricing of solicitors’ PII.

The 2018 and 2019 years are well developed and it is useful to note that of all the closed notifications, only a small percentage actually resulted in any payments being made. This highlights the fact that most notifications are precautionary or do not have the adverse outcome that was anticipated. It also highlights the importance of firms making precautionary notifications as underwriters expect to see a significant number of precautionary notifications that ultimately close without payment.

To the extent that your firm replicates this pattern of notifications, it will be beneficial to highlight when discussing claims and risk management with underwriters. Typically, if a firm notifies a high proportion of precautionary matters which are ultimately closed with no payments being required, underwriters are reassured that the firm has good risk management, which they consider positive and indicative of a healthy culture in the firm.

Conclusion

Whilst all legal professionals do their best to ensure the best outcome for their client, allegations of negligence are unfortunately an inevitable part of the job in the world we currently live in. As the economic challenges continue, we anticipate that there will be more focus on claims by clients looking for someone to blame when their financial position is not as they hoped it would be. Good risk management is imperative to ensure that law firms are as well protected as they can be – especially as law firms are usually the first to receive complaints or claims when the outcome is not what the client was looking for!

Abi Hammond Cert CII

Senior Claims Executive

Professional Indemnity Claims